If you’re ever delayed making a payment, you’ll notice that you must pay some interests that you didn’t account for. To tackle this you should consider an online accounting software to help you keep track of your payments, you will also be able to handle interests and organise any other accounting responsibilities you have.Now that you’ve implemented it into your business, let's take a look at what exactly are late payment interests?What are interests on late payments?This interest rate refers to the amount of money you would need to pay above the original amount that was due, it’s mandatory to pay the compensation for a delayed payment by paying a specific fee. Essentially, are you late paying your invoice or loan? Then you should expect an interest fee.When you have been given a ‘loan’ per-say, whether that be strictly monetary or provided with a payable service/product, then you would have signed a contract to agree to the terms of payment, which outlines when you must pay back the amount due, including any relevant fees and interests. If you manage to breach the contract, then you will be faced with a set of default interest charges that the beneficiary will have to correct.But why do these interests exist? Simply, if you don’t pay someone, it’s likely that they cannot pay another person/company. So interest rates act as compensation for any inconvenience caused.How to calculate interests on late payments?The interest rate a business can charge if another business is late paying for goods or a service is called ‘statutory interest - this is 8% plus the Bank of England base rate for business to business transactions.Calculating interest for a full year

Calculate daily interest

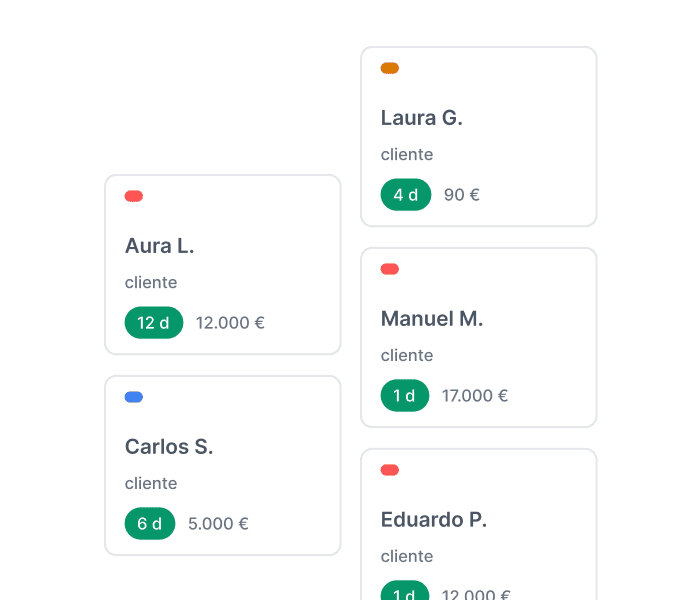

Calculate interest due by amount of late days

Do you have the right to charge interests on late payments?Every business has a statutory right to charge interest on late payments, this right applies to sales to business and public sector customers, but does not apply to sales to consumers.But should I charge interest rate? There are some things you should consider before doing so;

So if you decide that you should charge it, is completely your business’s decision. But if you do, use this article as your guide to how to calculate it. You can also take advantage of Holded’s accounting software to help you manage the recovery of payments.

.png)

.png)